This article is for educational purposes only and isn’t personalized financial advice. Stock prices, earnings figures, and analyst targets move fast to verify current numbers with your brokerage before making any trade.

Open ten different “best AI stocks” articles right now and you’ll find ten different lists, half of them quoting price targets that don’t trace back to anything real. That’s the problem with this keyword in 2026: the AI trade got so big, so fast, that the content trying to explain it got lazy right along with it.

So here’s a different approach. Every number in this guide comes from a company’s actual earnings filing, a named research firm, or reporting from outlets like CNBC and The Motley Fool, not a content farm’s guess at where a stock “could” go.

Here’s the thing: most “best AI stocks” content stops at the upside. This one doesn’t.

That’s what you’ll find in this guide to the best artificial intelligence stocks to buy in 2026: ten companies with real revenue tied to AI, a breakdown by category, an honest look at AI ETFs, and the risks nobody selling you a stock pick wants to slow down for.

Why Are AI Stocks Still Worth Looking At in 2026?

AI investing isn’t a story anymore. It’s a balance sheet line item at some of the largest companies on earth.

How big is the AI market actually?

According to Grand View Research’s 2026 industry report, the global AI market hit $390.9 billion in 2025 and is projected to reach $539.5 billion in 2026 then grow at a 30.6% compound annual rate through 2033, when it’s expected to top $3.5 trillion. North America holds about 35.5% of that market today.

Worth knowing: other research firms land on different numbers, because they don’t all count the same things as “AI.” MarketsandMarkets includes more hardware spend and lands closer to $602 billion for 2026. Mordor Intelligence’s figure is different again. None of them are wrong, exactly they’re just measuring different slices of the same elephant. Treat any single “$X trillion market” headline with a little skepticism, including this one.

Where the revenue is actually showing up?

This is the part that separates real AI investing from 2021-style speculation: the money is landing in earnings reports, not just keynote slides. Nvidia’s data center revenue alone hit $75.2 billion in a single quarter (more on that below) and that’s just one company. Add in Microsoft’s AI business, already running at a $37 billion annual revenue rate, and Palantir’s fastest quarterly growth since 2020, and a pattern shows up fast. These aren’t projections. They’re filed numbers.

Why does this work better as a long-term position than a trade?

AI stocks are volatile. Palantir alone is up roughly 23-fold since the end of 2022 and still dropped 18% earlier this year, according to CNBC’s coverage of its Q1 2026 earnings. If you’re chasing short-term moves in this sector, you’re competing against hedge funds with faster information and bigger risk tolerances than you. The case for AI stocks holds up better as a multi-year position in companies with durable, monetizing AI businesses, not a bet on next quarter’s headline.

How We Picked These 10 Stocks

No screener spit this list out. Each company made the cut because it cleared all five of these:

- Market leadership in a real AI value-chain segment (chips, cloud, software, or infrastructure)

- Revenue growth tied to AI specifically, not just “AI” in the earnings call transcript

- Balance sheet health cash flow and margins that can fund continued AI capex

- Analyst consensus that’s bullish for reasons beyond momentum

- A competitive moat that’s hard for a well-funded competitor to erase in 18 months

Companies that didn’t clear all five including a couple of small-cap names you’ve probably seen on other “best AI stocks” lists got cut. Having “AI” in the pitch deck was never one of the five.

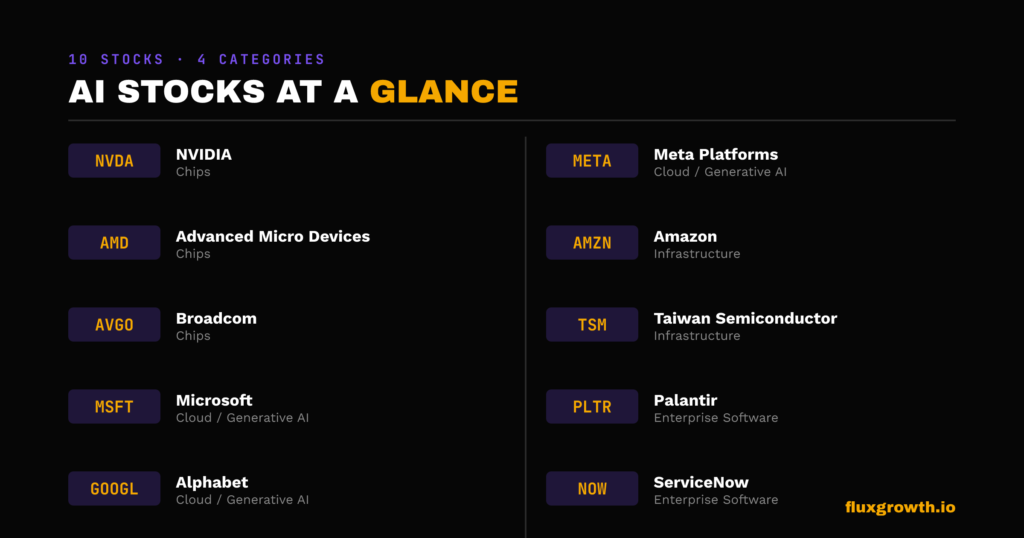

10 Best Artificial Intelligence Stocks to Buy in 2026

1.NVIDIA (NASDAQ: NVDA)

Nvidia is still the default answer to “what’s an AI stock,” and the numbers back it up. In its fiscal Q1 2027 results (reported May 20, 2026), Nvidia posted record revenue of $81.6 billion, up 85% year over year, with data center revenue alone hitting $75.2 billion up 92%. Full fiscal 2026 revenue came in at $215.9 billion, up 65% from the year before, per the company’s SEC filing.

That growth is coming from the ramp of Blackwell-generation chips and networking products like NVLink and Spectrum-X. Nvidia’s board also approved an additional $80 billion in share buybacks and raised the quarterly dividend from a penny to $0.25 per share, a sign management isn’t worried about cash.

The catch here is export controls. Nvidia took a $4.5 billion charge in fiscal 2026 after the U.S. government required new licenses for chip exports to China, and that policy can shift again with little warning. Valuation is also no longer cheap by any historical measure you’re paying up for the leader.

2.Microsoft (NASDAQ: MSFT)

Microsoft’s AI bet runs through two channels: its OpenAI stake and Azure. In the quarter ended March 2026, Microsoft’s revenue hit $82.9 billion, up 18% year over year, while Azure grew 40% an acceleration, not a slowdown. The company disclosed its AI business is now running at a $37 billion annual revenue rate, according to GeekWire’s reporting on the earnings call.

Microsoft owns roughly 27% of OpenAI and booked a $7.6 billion gain from that stake in a recent quarter. That’s a real accounting benefit, but it also means Microsoft’s results are now partly tied to a company it doesn’t control.

The crack in the story: OpenAI’s restructured agreement with Microsoft ended Azure exclusivity, meaning OpenAI can now run workloads on competing clouds like AWS. What used to be a closed loop now has a leak in it.

3.Alphabet (NASDAQ: GOOGL)

Alphabet’s AI story is Gemini plus an ad business that was supposed to be disrupted by AI chatbots and instead got reinforced by them. Google’s revenue grew 22% year over year with a 36% operating margin, according to The Motley Fool’s coverage of recent earnings, and the stock is up roughly 136% over the trailing year as of May 2026.

What’s notable: a year ago, the consensus was that ChatGPT would eat Google Search. Instead, Google’s AI Mode reportedly crossed 1 billion monthly active users within a year of launch. Despite the run, shares still trade at a forward P/E near 29 reasonable next to other mega-cap AI names.

The one thing to watch: advertising is cyclical, and Alphabet’s core revenue still leans heavily on it regardless of how much AI gets layered on top.

4.Amazon (NASDAQ: AMZN)

Amazon is the AI laggard among the hyperscalers in one specific way: it doesn’t have a leading large language model and got a late start on generative AI. But that misses where Amazon actually makes money on AI: infrastructure. AWS’s custom silicon business Graviton, Trainium, and Nitro chips combined is running north of $20 billion a year and growing at a triple-digit clip year over year, based on disclosures referenced in Arm’s most recent earnings report.

Amazon also booked a $16.8 billion pretax gain on its Anthropic stake in a recent quarter, per reporting on the company’s 10-Q filing the same pattern Microsoft is running with OpenAI.

There’s a bet within the bet here: without a flagship model, Amazon is betting that being the cheapest, most flexible place to run AI matters more than building the AI everyone talks about. So far, the AWS numbers say that bet is working but it’s a different bet than its peers are making.

5.Meta Platforms (NASDAQ: META)

Meta’s AI strategy is unusual: open-source the models, monetize the advertising. Meta’s Generative Ads Recommendation Model (GEM), trained across thousands of GPUs, is already showing up in the numbers and revenue grew 33% year over year in a recent quarter, with earnings up 62%, according to Yahoo Finance’s earnings coverage. Despite that growth, shares trade around 20 times this year’s earnings estimate, which is cheap relative to the growth rate.

Here’s the tension, though: Meta is spending enormous sums on AI infrastructure with a less obvious near-term payoff than a cloud provider that sells computers directly to customers. The advertising upside is real, but it’s also the only upside if the broader AI bet underdelivers.

6.Advanced Micro Devices (NASDAQ: AMD)

AMD is the credible “second source” in AI chips not a Nvidia replacement, but a real alternative that hyperscalers want to exist for negotiating leverage alone. The headline deal: OpenAI received warrants to buy a stake of roughly 10% in AMD at a penny a share. In exchange, OpenAI committed to 6 gigawatts of AMD Instinct GPUs, a deal AMD says represents up to $90 billion in cumulative hardware revenue potential, per reporting from analyst Tomasz Tunguz.

AMD’s MI350 chips, with 288GB of memory versus Blackwell’s 180GB, have already landed deployment commitments from Microsoft, Meta, and Oracle, per Seeking Alpha’s coverage. AMD’s market cap sat around $540 billion as of late April 2026, according to TradingKey’s analysis.

The honest caveat here: Nvidia still holds an estimated 80-95% share of the AI training chip market. AMD is gaining real ground, but it’s still playing from behind, and “$90 billion in potential revenue” is a multi-year ceiling, not a number that shows up in next quarter’s results.

7.Palantir Technologies (NASDAQ: PLTR)

Palantir had the strongest quarter of any company on this list. Q1 2026 revenue hit $1.63 billion, up 85% year over year its fastest growth since 2020 with U.S. commercial revenue up 133%. The company raised full-year guidance to roughly $7.65 billion, beating Wall Street’s prior estimate of $7.27 billion, according to multiple earnings reports including CNBC’s.

Here’s the catch: despite beating on every metric that matters, the stock fell nearly 6% after the print. Investors are pricing in near-perfect execution, and Palantir’s price-to-sales ratio has run as high as 80 to 100 a level The Motley Fool’s analysts have flagged as historically unsustainable for any company, regardless of growth rate.

Bottom line: this is the single most expensive way to buy AI growth on this list. If quarterly growth decelerates even modestly, the stock has a lot further to fall than slower-growing peers.

8.Broadcom (NASDAQ: AVGO)

Broadcom makes the custom AI chips ASICs, in industry shorthand that hyperscalers design in-house instead of buying off-the-shelf GPUs. It’s landed some of the largest deals in the business doing it: reportedly building custom accelerators for Google and Meta, plus a 10-gigawatt custom silicon deal with OpenAI.

How much is the OpenAI partnership worth? That’s less clear. Neither Broadcom nor OpenAI has disclosed financial terms. Some analysts estimate the deal could ultimately be worth hundreds of billions of dollars based on industry infrastructure costs, but those figures remain speculative rather than company-confirmed.

The vulnerability here is customer concentration. Broadcom’s AI business depends on a small number of enormous customers losing one major design win and the growth story changes fast.

9.Taiwan Semiconductor Manufacturing Company (NYSE: TSM)

Every AI chip designer on this list Nvidia, AMD, even Apple depends on TSMC to actually manufacture the silicon. That’s the whole investment case: TSMC doesn’t need to pick the winning AI chip architecture, because it gets paid regardless of which one wins. It’s the toll booth, not the racehorse.

The geography problem is the real risk here. The overwhelming majority of TSMC’s advanced manufacturing still happens in Taiwan, which means geopolitical risk around the Taiwan Strait is a real, non-theoretical input into this stock’s price, not a footnote.

10.ServiceNow (NYSE: NOW)

ServiceNow is the enterprise software bet on AI: instead of building AI models, it’s building the control layer that lets big companies actually deploy AI agents safely across existing workflows. Q1 2026 subscription revenue hit $3.67 billion, up 22% year over year, and the company raised full-year guidance to a midpoint near $15.76 billion, according to ServiceNow’s own SEC filing.

ServiceNow built an “AI Control Tower” to manage AI agents from any vendor, not just its own smart hedge given how fast the agent landscape is shifting.

The fine print: ServiceNow trades as a premium enterprise software name, and any slowdown in IT budgets would hit a stock priced for continued acceleration.

Best AI Stocks by Category

Best AI Chip Stocks

Nvidia, AMD, and Broadcom each play a different role in the same supply chain: Nvidia dominates general-purpose AI training GPUs, AMD is the credible alternative gaining real deployment commitments, and Broadcom builds the custom chips hyperscalers designed for their own specific workloads. If you only buy one chip stock, you’re picking a side. If you buy all three, you’re betting on AI chip demand broadly which has been the safer bet so far.

Best Generative AI Stocks

Microsoft, Alphabet, and Meta are the three companies actually shipping generative AI products at consumer and enterprise scale Copilot, Gemini, and Meta AI, respectively while also owning enough other revenue (cloud, search, advertising) to absorb the capex without betting the company.

Best AI Infrastructure Stocks

Amazon and TSMC sit a layer below the chip and software names one rents out the computer, the other manufactures the chips that make the computer possible. Neither needs you to guess which AI model or chip architecture wins.

Smaller, Higher-Risk AI Stocks — and a Word on “AI Penny Stocks”

Palantir is the smallest, most volatile name on the main list, and its valuation already reflects that risk.

If you’re searching for “AI stocks under $10,” be careful what you find.

Most genuinely sub-$10 AI-themed stocks are small-cap companies with limited revenue, inconsistent profitability, and significant price volatility. That’s not necessarily bad, but it’s the reality of this corner of the market. SoundHound AI (NASDAQ: SOUN) is one example. The stock surged from below $3 in 2023 to an all-time high above $24 during the AI boom before experiencing a sharp pullback. That kind of dramatic rise followed by equally dramatic declines is common among speculative AI stocks.

That round trip moonshot, then gut-check is the pattern with this category, not the exception. Treat low-priced AI stocks as speculation-sized positions, not core holdings. If you touch them at all.

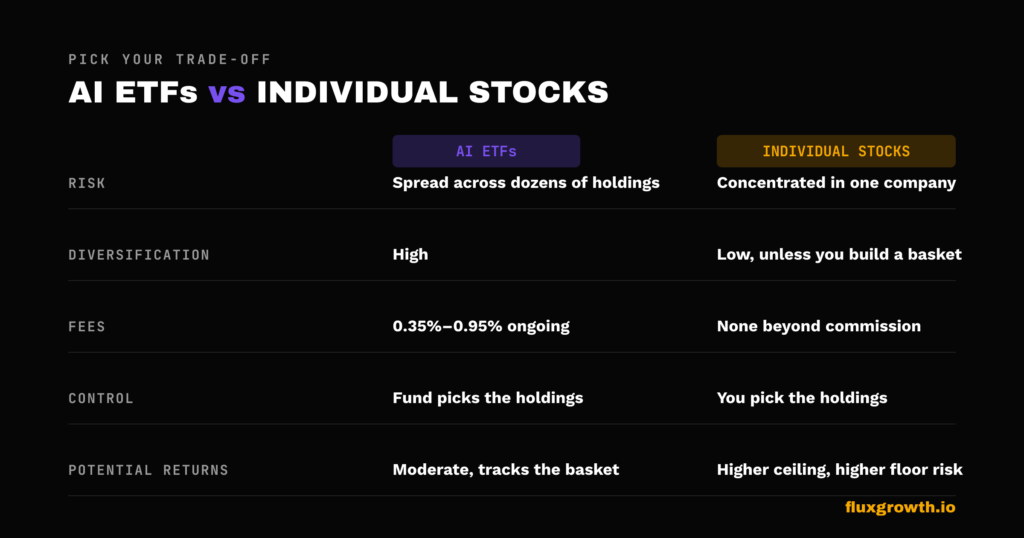

AI ETFs vs. Individual AI Stocks

If picking ten winners feels like more work than you want to do every quarter, AI-themed ETFs are a real alternative though they come with their own trade-offs.

| Feature | AI ETFs | Individual Stocks |

| Risk | Lower (spread across dozens of holdings) | Higher (concentrated in one company) |

| Diversification | High | Low, unless you build a basket yourself |

| Fees | 0.35%–0.95% expense ratio, ongoing | None beyond trading commission |

| Control | You own the fund’s choices | You own your choices |

| Potential returns | Moderate tracks the basket | Higher ceiling, higher floor risk |

A few real options, not hypotheticals.

AIQ (Global X AI & Technology ETF) is the largest dedicated AI fund roughly $9.5 billion in assets, 0.68% expense ratio, per U.S. News’ May 2026 coverage. The catch: it overlaps heavily with the Nasdaq-100. If you already hold QQQ, you might be paying an extra fee for stocks you already own.

CHAT (Roundhill Generative AI & Technology ETF) skips the diversification and makes a concentrated, actively chosen bet on generative AI specifically up 41.7% year-to-date as of May 2026, versus QQQ’s 14.1%. That kind of concentration cuts both ways in a downturn, sure, but it’s also exactly why it’s outperforming right now.

BOTZ goes the other direction: physical robotics and automation instead of software AI, with a steeper 0.95% expense ratio (the priciest of the bunch).

Want exposure to the chip layer without paying an “AI” markup for it? Semiconductor ETFs like SMH or SOXX charge roughly 0.34% — 0.35% and hold Nvidia, TSMC, and Broadcom anyway, same exposure, lower fee, no thematic label.

There’s no Vanguard-branded pure-play AI ETF as of this writing, despite how often people search for one.

The Real Risks of AI Stocks Right Now

This is the section most “best AI stocks” articles skip, because warning people doesn’t drive affiliate clicks. It should still be here.

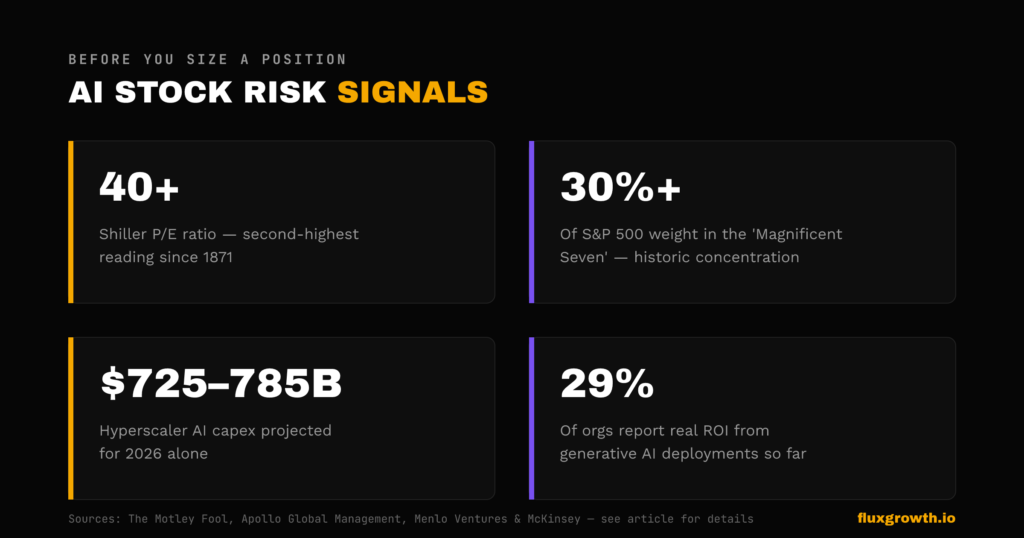

1.Valuations are stretched, and some serious people are saying so out loud:

Goldman Sachs’ own head of global equity research, James Covello, has publicly questioned the AI trade’s trajectory from inside Goldman. Michael Burry, the investor who famously called the 2008 housing crash, has taken a leveraged short position via options on the semiconductor ETF SOXX, according to reporting on his recent investor letters.

Then there’s the Shiller P/E. The S&P 500’s reading crossed 40 earlier this year, the second-highest level since 1871. Only two other times has it broken 40. Both ended badly: down 49% after the dot-com crash, down 25% in the 2022 bear market, per The Motley Fool’s analysis. Two for two isn’t a great track record to bet against.

2.Concentration risk is historically high:

The “Magnificent Seven” tech stocks now make up more than 30% of the S&P 500’s total weight, the highest concentration in decades, according to Apollo Global Management’s chief economist. Buying an S&P 500 index fund today gives you far less diversification than it would have five years ago, even though it still feels like “buying the whole market.”

3.Capex is enormous, and the ROI question is still open:

Hyperscalers are projected to spend somewhere between $725 billion and $785 billion on AI infrastructure in 2026 alone, by some estimates rising toward $1 trillion in 2027. Meanwhile, research cited in 2026 coverage from Menlo Ventures and McKinsey found only 29% of organizations report seeing significant ROI from their generative AI deployments so far. Spending and payoff are not currently moving at the same speed.

4.Sentiment can flip fast, with real consequences:

When the DeepSeek model emerged in early 2025 showing comparable performance at a fraction of the cost, Nvidia’s stock dropped 17% in a single session to about $600 billion in market value in a day, per widely reported coverage at the time. That’s not ancient history. It’s a preview of what a single piece of unexpected news can do to a sector this concentrated.

5.Regulatory and export-control risk is ongoing, not resolved:

Nvidia’s $4.5 billion China-related charge wasn’t a one-time event; it’s a structural risk that applies to every chipmaker with meaningful exposure to AI exports, and policy can change with a single announcement.

None of this means avoiding AI stocks. It means size your positions like someone who’s read this section, not someone who skipped to the buy list.

How to Actually Buy AI Stocks

If you’ve never bought individual stocks before, the mechanics are simpler than the research:

- Open a brokerage account — most major brokers (Fidelity, Schwab, E*TRADE) now offer commission-free trades and fractional shares, so you don’t need $215 to buy one NVDA share outright.

- Decide stock vs. ETF vs. both — based on how much individual research you actually want to do every quarter.

- Size the position before you buy it, not after deciding what percentage of your portfolio any single AI stock or ETF will represent, and stick to it.

- Use dollar-cost averaging for a volatile sector like this one buying a fixed dollar amount on a schedule smooths out the kind of single-day swings this list has already shown you.

- Read the actual earnings release, not just the stock-price reaction, every quarter you hold the position. Palantir’s stock fell after a genuinely great quarter; the headline price move and the underlying business news aren’t always the same story.

What I’d Do If I Were Starting Today

If I were starting to invest in AI today, I wouldn’t chase whichever stock is trending on social media. I’d begin with established companies like NVIDIA, Microsoft, and Alphabet because they already have profitable businesses, strong balance sheets, and significant investments in AI infrastructure.

I’d also consider starting with an AI-focused ETF to gain diversified exposure rather than putting all my money into a single stock. Once I had a better understanding of the sector, I’d gradually explore higher-risk opportunities like Palantir or smaller AI companies.

A framework I’d consider is a core-and-satellite approach: keep most of an AI allocation in diversified, established businesses such as Microsoft, Alphabet, and Amazon, where AI is only one of several growth drivers. A smaller portion could go toward higher-growth, higher-volatility names like NVIDIA, AMD, or Palantir, while speculative small-cap AI stocks should make up only a very small part of a portfolio, if any.

The biggest lesson? Focus on the business, not the hype. AI is a long-term trend, and successful investing usually comes from owning quality companies for years rather than trying to predict short-term price movements.

Disclaimer: This article is for educational and informational purposes only and should not be considered financial or investment advice. Always conduct your own research and consult a qualified financial advisor before making investment decisions.

Expert Tips for Investing in AI Stocks

- Focus on fundamentals, not narrative. “AI company” isn’t a moat. Ask what specific, monetizing problem the AI solves and who’s already paying for it.

- Avoid hype-driven investing. If a stock’s main investment thesis is “everyone’s talking about it,” that’s not a thesis check the actual revenue numbers in this guide before you act on a headline.

- Diversify across the AI value chain, not just across individual stocks. Chips, cloud, software, and infrastructure don’t all move together, which matters when one segment has a rough quarter.

- Think in years, not earnings cycles. Palantir’s stock dropped right after a beat-and-raise quarter; that’s the noise a long-term thesis is built to ignore.

Frequently Asked Questions

What is the best artificial intelligence stock to buy?

There isn’t one “best” AI stock, it depends on your risk tolerance. Nvidia has the strongest current AI-specific revenue and growth of any large-cap name. Microsoft and Alphabet offer more diversified, lower-volatility exposure to the same trend.

Which AI stock has the most growth potential?

By percentage growth, Palantir’s 85% year-over-year revenue growth in Q1 2026 outpaced every other large-cap name on this list but that growth comes with the highest valuation risk of the group, too.

Are AI stocks a good investment in 2026?

The sector has real, growing revenue behind it now, not just hype but valuations are historically stretched by several measures, and respected analysts are openly debating bubble risk. “Good investment” depends heavily on your time horizon and position sizing, not just which stocks you pick.

What are the top AI stocks for beginners?

Microsoft, Alphabet, and Amazon are generally considered lower-volatility entry points because AI is one growth driver among several diversified, profitable businesses rather than the entire investment thesis, as it is with Palantir or smaller AI-pure-play names.

Is NVIDIA still a good AI stock to buy?

Nvidia’s fundamentals remain the strongest on this list by revenue and growth. The open questions are valuation and export-control policy risk, not whether the underlying business is real.

What are the risks of investing in AI stocks?

Stretched valuations, historic market concentration in a handful of tech names, enormous capex with still-unproven ROI at scale, fast sentiment shifts (see: Nvidia’s 17% one-day drop after the DeepSeek news), and ongoing regulatory and export-control uncertainty.

Should I buy AI ETFs or individual stocks?

ETFs trade a lower ceiling for a lower floor. You get instant diversification and skip the quarterly research, but you also pay an ongoing fee and dilute your exposure to whichever single stock might outperform. A blended approach, a core ETF position plus one or two individual stocks you’ve actually researched is a reasonable middle ground for most people.

If there’s one thing every number in this guide points to, it’s this: the best artificial intelligence stocks to buy in 2026 are the ones with revenue that’s already real, not just a story about where revenue might show up someday. AI is no longer a bet on a future technology, it’s a bet on whether today’s prices already assume that future arrived. Decide which side of that bet you’re actually making before you click buy.

1 thought on “Best Artificial Intelligence Stocks to Buy in 2026”